Yes, blockchain is a type of distributed ledger. A distributed ledger is a database that is replicated and shared across multiple nodes or computers in a network. Each node in the network maintains a copy of the ledger and independently verifies and updates it through a consensus mechanism.

Blockchain technology utilizes a distributed ledger to store and validate transactions or information in a decentralized manner. It achieves consensus among participants through cryptographic algorithms, allowing them to agree on the state of the ledger without the need for a central authority.

In a blockchain, transactions are grouped into blocks, and each block is linked to the previous block, forming a chain of blocks. This chain of blocks, known as the blockchain, maintains a chronological record of all transactions or data ever added to it. The distributed nature of the blockchain ensures that all participants have access to the same information and can independently verify the integrity of the ledger.

So, in summary, blockchain is a specific implementation of a distributed ledger that uses cryptographic techniques and consensus mechanisms to create a decentralized and tamper-resistant system for recording and verifying transactions or data.

Additional points about blockchain as a distributed ledger:

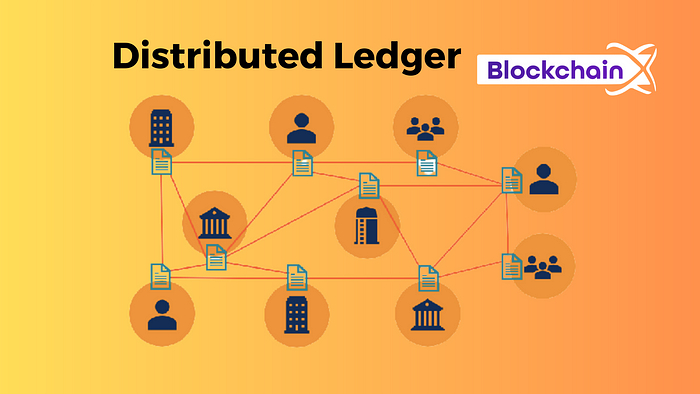

Distributed Ledger:

Blockchain technology utilizes a distributed ledger to store and validate transactions or information in a decentralized manner. It achieves consensus among participants through cryptographic algorithms, allowing them to agree on the state of the ledger without the need for a central authority.

In a blockchain, transactions are grouped into blocks, and each block is linked to the previous block, forming a chain of blocks. This chain of blocks, known as the blockchain, maintains a chronological record of all transactions or data ever added to it. The distributed nature of the blockchain ensures that all participants have access to the same information and can independently verify the integrity of the ledger.

So, in summary, blockchain is a specific implementation of a distributed ledger that uses cryptographic techniques and consensus mechanisms to create a decentralized and tamper-resistant system for recording and verifying transactions or data.

Additional points about blockchain as a distributed ledger:

- Immutability: Once a block is added to the blockchain, it is extremely difficult to alter or delete the information stored within it. The use of cryptographic hash functions and the decentralized nature of the network make it highly resistant to tampering, providing a high level of data integrity.

- Transparency: Blockchain networks are often designed to be transparent, allowing all participants to have visibility into the transactions and data stored on the ledger. Depending on the blockchain’s configuration, participants can view and verify the entire transaction history, enhancing trust and accountability within the network.

- Decentralization: In a blockchain network, there is no central authority controlling or governing the system. Instead, control is distributed among multiple nodes, making it more resilient to failures or attacks. This decentralized nature also reduces the reliance on intermediaries and can enable peer-to-peer transactions without the need for intermediaries such as banks or clearinghouses.

- Consensus Mechanisms: Blockchain networks employ consensus mechanisms to agree on the state of the ledger and validate transactions. Different blockchain platforms use various consensus algorithms, such as Proof of Work (PoW), Proof of Stake (PoS), or Byzantine Fault Tolerance (BFT), to achieve agreement among participants and maintain the integrity of the ledger.

- Smart Contracts: Blockchain technology often includes the capability to execute smart contracts. Smart contracts are self-executing agreements with predefined rules and conditions. They automatically trigger actions or transactions when certain conditions are met, eliminating the need for intermediaries and enhancing the efficiency of business processes.

- Applications beyond cryptocurrencies: While blockchain technology gained prominence with the advent of cryptocurrencies like Bitcoin, its potential applications extend far beyond digital currencies. Blockchain can be utilized in various industries and use cases, including supply chain management, healthcare, finance, voting systems, intellectual property, and more, to improve transparency, security, and efficiency.

Distributed Ledger:

- A distributed ledger is a database that is replicated and shared across multiple nodes or computers in a network.

- It allows participants in the network to independently maintain a copy of the ledger and verify and update it through a consensus mechanism.

- The ledger can be decentralized or partially decentralized, depending on the specific implementation.

- The ledger can store various types of information, such as transactions, contracts, or other data, depending on the use case.

- Examples of distributed ledger technologies include blockchain, directed acyclic graph (DAG) systems, and other forms of distributed databases.

- Blockchain is a specific type of distributed ledger that utilizes cryptographic techniques to create a decentralized and tamper-resistant system.

- It is characterized by the chaining of blocks, where each block contains a set of transactions or data and is linked to the previous block.

- The blocks are added to the chain through a consensus mechanism, which ensures agreement among participants about the validity of transactions and the state of the ledger.

- Blockchain technology provides transparency, immutability, and security through its design and cryptographic algorithms.

- Blockchain is often associated with cryptocurrencies like Bitcoin, but it has broader applications beyond digital currencies.